In This Article

- What changed, and why it matters now

- Where the EX‑FILING FEES exhibit fits

- A tale of two filing days

- What must be tagged, and what commonly goes wrong

- How to build a smoother workflow without slowing the deal

- Investment company specifics: identifiers, enumerations, and reorganizations

- Looking ahead to July 31, 2025, and after

If your SEC submission includes filing fees, your process just gained a new, non‑negotiable step. Beginning July 31, 2025, the Inline XBRL fee tagging exhibit, EX‑FILING FEES, is required for all filers, including operating companies with fee‑bearing registrations and certain investment companies using Forms N‑2 and N‑14.

It’s part of the SEC’s push to make fee disclosures structured, machine‑readable, and readily validated. That’s good for long‑term accuracy. It also means EDGAR will be less forgiving of small mistakes that once slipped by, like entering decimal values where the schema expects whole integers.

Think of the exhibit as a mirror held up to your fee table: the same underlying facts, encoded in Inline XBRL so EDGAR can validate both math and structure.

You’re not writing more disclosure; you’re expressing the same details with more precision, clean data types, consistent identifiers, and correct rule references. With a good workflow, this becomes routine. With a rushed one, it becomes a bottleneck.

What changed, and why it matters now

Historically, fee disclosures lived in tables and paragraphs inside registration statements and prospectus materials, while payment logistics happened in parallel.

The SEC’s fee disclosure and payment modernization pulls more of that into a structured layer. Inline XBRL makes the data traceable and comparable, enabling automated validations that flag inconsistencies in seconds.

For issuers, the critical risk is timing: a takedown that must price tonight cannot absorb an EDGAR rejection over a mis‑tagged share count. For funds, the challenge is consistency: series and class identifiers in N‑2 or N‑14 must match the EX‑FILING FEES exhibit precisely.

To strengthen your foundation, it helps to revisit the essentials of XBRL Filing so your team understands what the tags are doing under the hood.

Make Your Next SEC Filing the Easiest One Yet

Join hundreds of satisfied clients who trust our responsive team for their EDGAR/iXBRL filings, newswire, and financial printing needs.

Where the EX‑FILING FEES exhibit fits

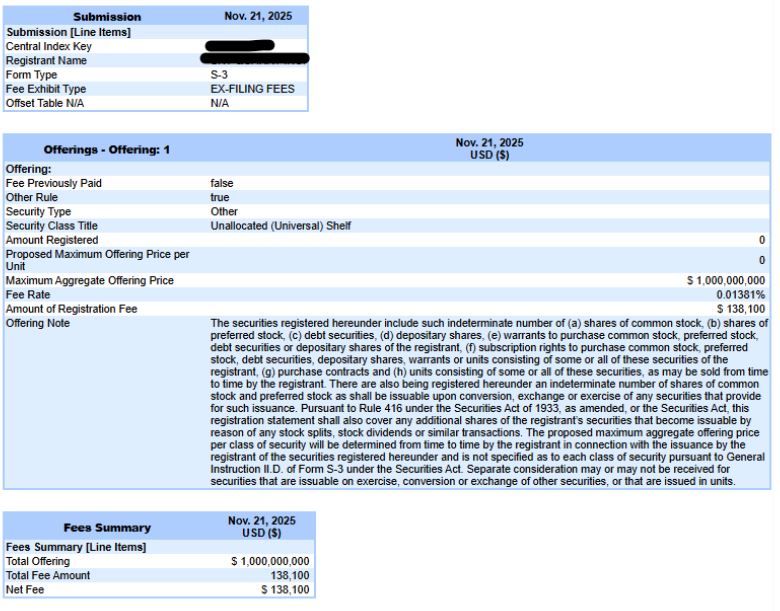

The exhibit sits alongside your narrative disclosure. It doesn’t replace the prospectus fee table or the discussion of rules invoked, think Rule 457(c) for market price, 457(o) for aggregate offering price, 457(r) for automatic shelf registration, and 457(p) for fee offsets.

Instead, it encodes the same elements in Inline XBRL: security titles and identifiers; price or aggregate amount; the applicable fee rate; the calculated fee; and any offsets or carryforwards with precise cross‑references to prior file numbers.

As you formalize this step, consider where your Edgar Services partner plugs in; quality control over data types, rule mapping, and pre‑validation often makes the difference between a smooth acceptance and a last‑minute scramble.

A tale of two filing days

Picture a mid‑cap issuer preparing an overnight S‑3 takedown. In the old world, the fee table got a careful review, numbers rolled forward from working papers, and the EDGARization team ensured the exhibit matched the narrative.

In the new world, the Inline XBRL layer enforces its own rules. One team caught a count field tagged as “1.00” instead of “1” and an outdated 457(p) file number during pre‑validation. Ten minutes of repair preserved the pricing window. Without that run, the rejection would have hit just as counsel was ready to push live.

For a fund reorganization on Form N‑14, the story rhymes: the math was correct, but the exhibit used a slightly different class name than the body of the filing.

EDGAR flagged the mismatch. A quick identifier audit, a re‑tag, and acceptance arrived on the second attempt. Tight alignment between the exhibit and the narrative is no longer a best practice; it’s a gating item.

What must be tagged, and what commonly goes wrong

Every filing is unique, but the EX‑FILING FEES exhibit generally covers the same ground: the title of each class of securities; the calculation basis under the applicable rule; the fee rate and result; and any fee offsets and carryforwards with prior‑file references. Funds add the wrinkle of series and class identifiers, which must be consistently applied across the entire filing set. What trips filers up isn’t obscure; it’s mundane.

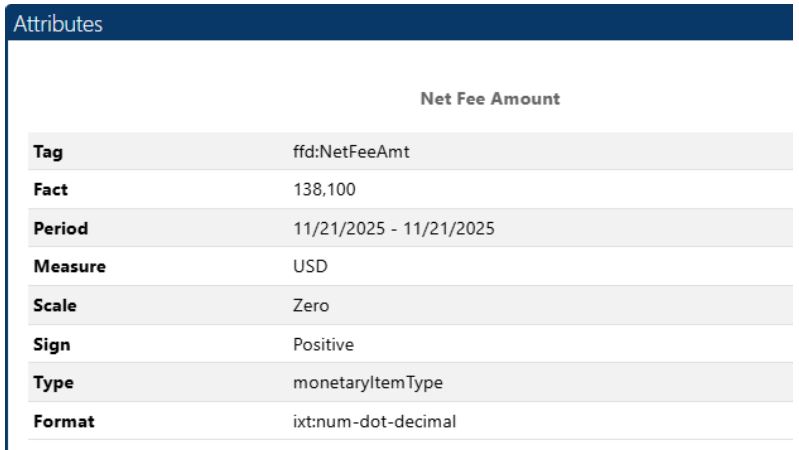

The examples below show how these XBRL tagging attributes appear in the filing when the linked amount is expanded:

- Maximum Aggregate Offering Price:

- Fee Rate:

- Net Fee Due:

- EDGAR pre-validation results screen highlighting a currency or rule-basis warning and its fix.

Some fields accept only integers, share counts, for example, while others accept currency with precision. A misplaced decimal, a pre‑scaled “thousands” assumption, or a USD tag that doesn’t match the narrative can all cause pain. Offsets are another frequent snag: if you’re drawing on a prior registration under Rule 457(p), the exhibit must point precisely to the source, file number, date, and remaining balance before and after the draw, so your SEC Filing Services process should maintain an offsets ledger you can trust.

| Common error | How to spot it | Fix |

| Integers entered as decimals | Share counts show “1.00” or any decimal precision | Enter whole numbers only; remove decimals and thousand separators |

| Wrong rule basis (457(c) vs 457(o)) | The fee doesn’t reconcile to the calculation method described | Confirm the transaction facts; select the rule that matches your price basis |

| Mis-tagged currency | Narrative uses USD, exhibit uses a mismatched currency tag | Set currency to USD and align with narrative and working papers |

| Missing 457(p) cross-references | EDGAR flags a missing or invalid prior file number/date | Tag the prior file number, date, and offset amount precisely |

| Series/class ID mismatch (funds) | IDs in the exhibit differ from those in the body of the filing | Sync identifiers across the filing package, then re-validate |

| Pre-scaled values | Amounts appear 1,000x too big or small | Enter exact values; don’t pre-scale unless the schema explicitly allows it |

How to build a smoother workflow without slowing the deal

Treat the exhibit as an extension of your fee calculation process, not a separate project. Start with sound working papers: a short memo recording the rule selection (e.g., 457(c) for a market‑priced equity offering) and the numbers tied to that choice, plus any offsets you intend to use. Then map those exact facts into the Inline XBRL exhibit, one figure at a time, one tag at a time.

If the narrative table says “25,000 warrants,” the exhibit should reflect a count of 25000 with no decimals and the same security title. Run a pre‑validation through EDGAR and leave time for the loop: validate, fix, validate again. Once the exhibit clears cleanly, archive the calculations and cross‑references for the next amendment or takedown. Because offerings often coordinate with operational rails, it’s wise to confirm settlement readiness items like DTC Eligibility during planning so nothing downstream disrupts your filing window.

Investment company specifics: identifiers, enumerations, and reorganizations

Closed‑end funds and BDCs filing on Forms N‑2 and N‑14 face the same core requirement with extra attention to identifiers. Series and class IDs must match everywhere, exactly.

Reorganizations can alter the fee base, so double‑check that the enumerations you select in the exhibit match the structure described in the body text. Treat series/class IDs as master data with a single source of truth across your documents and tags. And if your capital plan intersects with exchange readiness, a quick reconfirmation of Nasdaq listing requirements during calendar planning can help align disclosure timing with market objectives.

A concise pre‑filing checklist

- Facts documented: security titles, counts, price basis, and rule selection.

- Offsets ledger current: prior file numbers, dates, amounts, and remaining balances.

- Exhibit mapped from the narrative table: one figure to one tag, correct data types and currency.

- EDGAR pre‑validation run completed; errors resolved and a clean pass achieved.

- Working papers archived for future amendments and audits.

Looking ahead to July 31, 2025, and after

This requirement applies to all filers beginning July 31, 2025. Expect refinements as the SEC tunes validation and guidance. The path of least resistance is to stay close to the official materials, the EDGAR Filing Fee Interface Courtesy Guide for field definitions and data‑type rules, and the SEC’s EDGAR Filing Fees hub for FAQs and schema updates, and to treat each validation message as an opportunity to tighten your guardrails.

By integrating fee tagging into your routine working papers now, you reduce risk on filing day and speed every future amendment.

For compliant EX‑FILING FEES exhibits and Inline XBRL tagging aligned with EDGAR validation, contact Colonial Stock’s SEC filing services team.