XBRL, or eXtensible Business Reporting Language, has revolutionized financial transactions worldwide. It began as a niche technology in the late 1990s, first introduced by the American Institute of Certified Public Accountants (AICPA) after using XML (eXtensible Markup Language) to automate financial reporting. He recognized its potential to standardize and streamline the exchange of financial information across different software and platforms. The idea quickly caught on when the SEC adopted it in 2005 and has since become a global standard for digital business reporting, facilitating the efficient, accurate, and transparent exchange of financial information among businesses, regulatory bodies, and stakeholders. With its robust capabilities, XBRL ensures semantic interoperability, allowing seamless communication across diverse systems and jurisdictions.

Understanding XBRL

XBRL is an open international standard designed for digital business reporting. It provides a framework for preparing, exchanging, and analyzing financial reports in a machine-readable format. Whereas traditional methods of financial reporting (e.g., Hyper Text Markup Language) frequently rely on static formats like PDF or Excel, XBRL allows for dynamic, machine-readable data that can be automatically processed and analyzed. XBRL gives each piece of financial data a unique identifier, known as an XBRL tag, making it easily accessible and analyzable by computers.

The Role of XBRL Tags

XBRL operates on a tagging system where specific labels are attached to different elements of financial data. These tags describe the nature of the data, such as sales figures, net assets, or accounting policies, using a standardized vocabulary. This vocabulary is defined within an XBRL taxonomy, which is essentially a set of concepts and rules that provides a framework for the specific data being reported.

Types of XBRL Taxonomies

Here is a list of the XBRL taxonomies that are used in most SEC filings to date. These taxonomies are developed and maintained by organizations such as the FASB and other regulatory agencies.

- US GAAP Taxonomy: The US GAAP (Generally Accepted Accounting Principles) Taxonomy is used by U.S. companies to report their financial data in accordance with the accounting standards set by the Financial Accounting Standards Board (FASB). It includes elements that reflect the specific reporting requirements of U.S. public companies, such as balance sheets, income statements, and cash flow statements. This taxonomy ensures that financial statements submitted to the SEC are consistent and easily comparable across companies.

- International Financial Reporting Standards (IFRS) Taxonomy: The IFRS Taxonomy is designed for companies that report their financials based on the International Financial Reporting Standards, which are used in over 140 jurisdictions worldwide. Managed by the IFRS Foundation, this taxonomy helps companies prepare financial reports that comply with international standards, ensuring global consistency and comparability across markets. It includes elements for both general-purpose financial statements and industry-specific reporting.

- Mutual Funds Risk/Return Summary (RR) Taxonomy: The Mutual Funds Risk/Return Summary (RR) Taxonomy is specifically created for the U.S. mutual fund industry. It facilitates the reporting of mutual fund performance, risk, and return information in a structured format. This taxonomy is used to ensure investors have access to clear and standardized data regarding mutual fund offerings, including historical returns, investment objectives, and fees, enabling better-informed investment decisions.

- Self-Regulatory Organizations (SRO) Taxonomy: The Self-Regulatory Organizations (SRO) Taxonomy is developed for use by entities such as exchanges, broker-dealers, and clearinghouses that self-regulate certain aspects of financial markets. This taxonomy supports the filing of reports related to compliance, market surveillance, and operational performance. It ensures that regulatory filings are structured in a standardized manner, promoting transparency and accountability within financial markets.

- Record of Ratings Taxonomy: The Record of Ratings Taxonomy is used by credit rating agencies to report and disclose their credit ratings for various financial instruments. This taxonomy provides a standardized way to document the ratings given to securities, helping investors and regulators track creditworthiness and risk exposure. It improves transparency in the credit rating process and makes it easier for market participants to access and analyze rating information across different agencies.

Here is the typical structure of what an XBRL taxonomy looks like:

| Component | Description |

| Elements | The individual tags used to label data |

| Attributes | Additional information that specifies how the data should be interpreted |

| Linkbases | Define the relationships between different elements |

| Dimensions | Allow for more complex data modeling, such as segment reporting |

Make Your Next SEC Filing the Easiest One Yet

Join hundreds of satisfied clients who trust our responsive team for their EDGAR/iXBRL filings, newswire, and financial printing needs.

Key Features of XBRL

1. Improved Data Accuracy and Reliability

One of the most significant advantages of XBRL is its ability to enhance the accuracy and reliability of financial data. By employing a standardized format, the potential for human error is minimized, as the data is automatically extracted and processed by XBRL-aware applications. This precision ensures that stakeholders have access to trustworthy information.

2. Enhanced Analysis and Comparability

XBRL facilitates better analysis of financial data by enabling users to compare information across different companies, industries, and regions. The standardized nature of XBRL makes it easier for analysts and investors to conduct comparative studies, thus supporting informed decision-making.

3. Global Interoperability

Given that XBRL is a globally recognized standard, it promotes interoperability among jurisdictions and systems such as the SEC, the FASB, NASDAQ, NYSE, and more. This characteristic is particularly beneficial for multinational companies and investors who need to analyze financial data from various countries with differing reporting standards.

4. Cost Efficiency

By streamlining the reporting process, XBRL can significantly reduce the costs associated with financial reporting. Companies can streamline their filing processes and data collection and processing, leading to faster reporting times and lower administrative burdens.

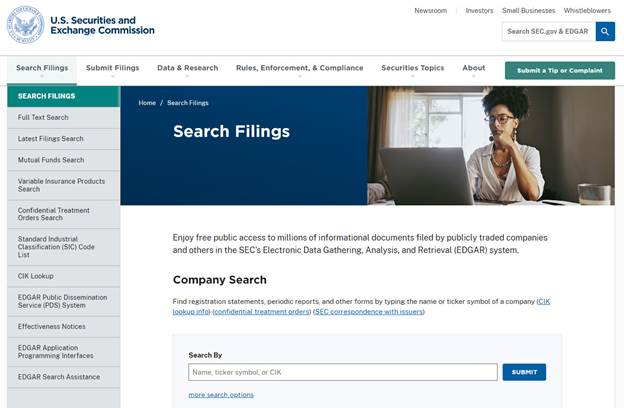

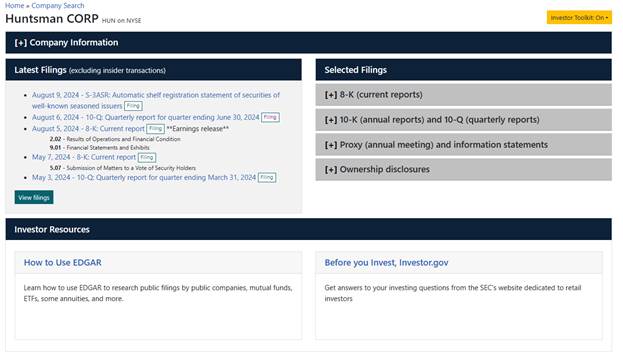

How to Download XBRL Data from an SEC Filing

-

- Go to the SEC’s EDGAR Database: Visit the SEC’s EDGAR search tool (https://www.sec.gov/search-filings).

- Search for the Company: Enter the company’s name or ticker symbol in the search box.

- Find the Filing: Look through the search results and click on the desired filing (e.g., 10-K, 10-Q).

- Access the Filing: On the filing’s summary page, look for the “Interactive Data” or “Documents” section.

- Download XBRL Data: Click on the XBRL files (often with extensions like .xml, .xsd, or .zip) and download them to your computer.

- Go to the SEC’s EDGAR Database: Visit the SEC’s EDGAR search tool (https://www.sec.gov/search-filings).

XBRL and Regulatory Compliance

With the increasing emphasis on transparency and accountability in corporate reporting, regulatory bodies around the world have started adopting XBRL as part of their reporting requirements. In the United States, publicly traded companies are mandated to file their financial statements in a new iXBRL (inline XBRL) format that includes both HTML and XBRL format, making it easier for the Securities and Exchange Commission (SEC) to analyze and review corporate financial data.

History of XBRL Implementation

Prior to 2009, financial statements were primarily submitted in HTML format, which was less structured and challenging for software to process. The SEC’s introduction of XBRL requirements marked a significant shift in how financial data was reported. From 2009 onward, companies were required to tag their financial statements with XBRL tags, which allowed machines to process the information more efficiently and effectively.

Here is a historical timeline of XBRL launching in the US for all SEC public company filings:

| Year | Event |

| 1998 | The concept of XBRL was introduced by Charles Hoffman |

| 2000 | XBRL International, a global consortium, is formed |

| 2003 | First XBRL instance document filed by a public company |

| 2009 | U.S. SEC mandates XBRL for public companies |

| 2013 | XBRL becomes mandatory for EU-listed companies |

| 2020 | Introduction of XBRL GL (Global Ledger) for internal use |

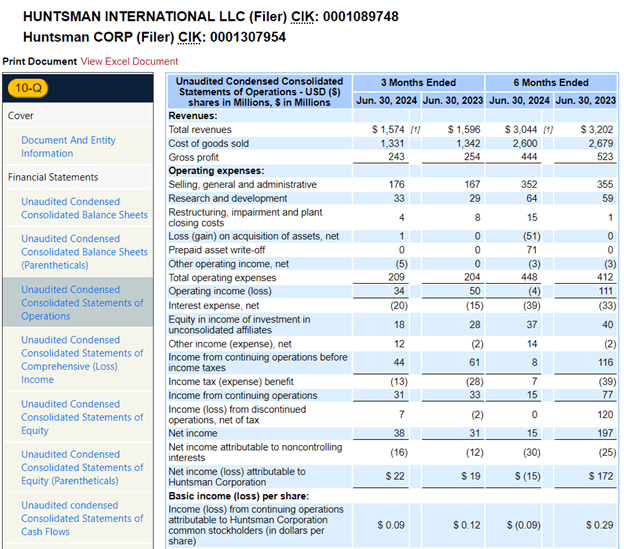

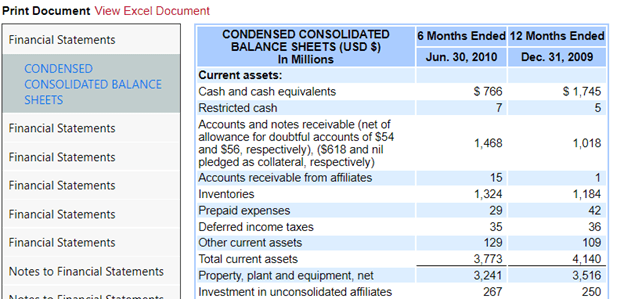

2010 Filing with regular XBRL in its early days:

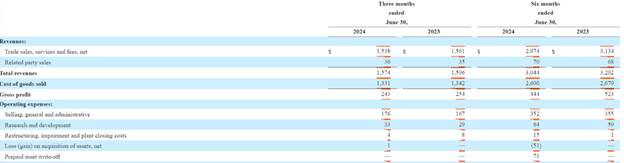

2024 Filing with inline XBRL (iXBRL):

iXBRL

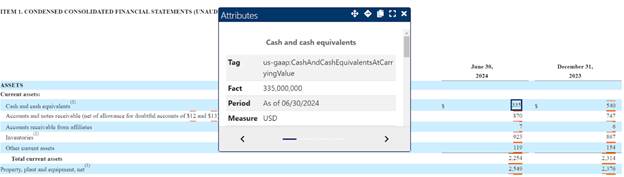

iXBRL (Inline eXtensible Business Reporting Language) is an enhanced version of XBRL. Whereas XBRL is solely machine-readable, iXBRL is both human-readable and machine-readable. It achieves this through integrating XBRL tags within an HTML document. This allows a user to view the document as a regular webpage while also allowing computers to extract and interpret the tagged financial data.

Here is an example of an iXBRL tag below with the tags highlighting numbers in red:

Challenges and Future of XBRL

Despite its many advantages, the implementation of XBRL does pose certain challenges. One major concern is the complexity involved in tagging financial data correctly. Companies may need to invest in training and software to ensure accurate tagging and compliance with XBRL specifications. Furthermore, as technology continues to evolve, the XBRL framework must adapt to keep pace with new developments, such as artificial intelligence and data analytics.

The future of XBRL is bright as more organizations recognize the need for structured, machine-readable formats in financial reporting. As data analytics and visualization tools become more prevalent, XBRL will likely play a pivotal role in transforming how financial information is consumed and analyzed. The ongoing development of XBRL taxonomies to accommodate emerging reporting standards will further enhance its relevance in the digital age.

Conclusion

In summary, XBRL represents a significant advancement in financial reporting, facilitating a more efficient, accurate, and transparent exchange of financial information. As the global business landscape continues to evolve, the adoption of XBRL will likely become increasingly important for organizations seeking to enhance their reporting processes and meet regulatory requirements. By embracing XBRL, businesses can position themselves for success in an increasingly data-driven world.